EN

EN ES

ES FR

FR PT

PT NL

NL DE

DE RU

RU SL

SL SV

SV TR

TR

By Pam Martens and Russ Martens,

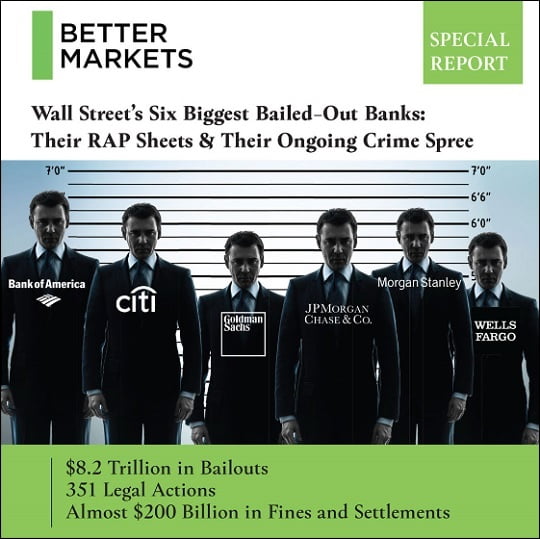

One day before Democrats on the House Financial Services Committee held an historic grilling of the CEOs of the mega banks on Wall Street, the nonprofit watchdog, Better Markets, released an in-depth research report on “Wall Street’s Six Biggest Bailed-Out Banks: Their RAP Sheets & Their Ongoing Crime Spree.” The report detailed facts, figures and this inescapable conclusion:

“[Six Wall Street mega banks] have engaged in—and continue to engage in—a crime spree that spans the violation of almost every law and rule imaginable. Taking the breadth and depth of their illegal conduct as a whole, the six biggest banks in the country look like criminal enterprises with RAP sheets that would make most career criminals green with envy. That was the case not just before the 2008 crash, but also during and after the crash and their lifesaving bailouts…In fact, the number of cases against the banks has actually increased relative to the pre-crash era.”

The six mega banks profiled in the report are: Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Wells Fargo.

A reliable source tells us that all major business media received the report on Tuesday, April 9. We know that Politico had the report by 8:00 a.m. because its “Morning Money” column provided a small news nugget at that time announcing that the report was out. Politico did not follow up, however, with any detailed coverage of the shocking revelations in the report.

Wall Street On Parade, after carefully reading and digesting the report, published an article on its contents the next morning, April 10. Then we began to hear from our outraged readers, who wanted to know why they weren’t reading about this report at major business media outlets. We checked the Wall Street Journal, the New York Times, Financial Times, Bloomberg News, Reuters, CNBC, and CNN. We could find no mention of the Better Markets report. (We checked again this morning. There is still a news blackout.)

We know that the Wall Street Journal was aware of the report because Lalita Clozel, a banking regulation reporter for the Wall Street Journal, Tweeted on April 10 that Democrats in the House Financial Services Committee room were handing out the report to journalists while the Chair of the Committee, Congresswoman Maxine Waters, was introducing the bank CEOs.

There are four words in this outstanding report from Better Markets that rendered it unpalatable to corporate business media: “rap sheets” and “criminal enterprise.” We searched Bloomberg News, the Wall Street Journal and the New York Times back to 2004 to see if at any time they had used the words “rap sheet” to describe the unprecedented serial crime sprees of these Wall Street mega banks. They had not. We did find this reference to rap sheets at the Wall Street Journal in 2014:

“Over the past 20 years, authorities have made more than a quarter of a billion arrests, the Federal Bureau of Investigation estimates. As a result, the FBI currently has 77.7 million individuals on file in its master criminal database—or nearly one out of every three American adults.”

Despite almost one-third of American adults having been arrested, not one CEO or top executive of the serially charged mega banks has seen the inside of a jail cell, despite criminal referrals from the Financial Crisis Inquiry Commission.

Wall Street On Parade has been regularly using the phrase “rap sheet” since 2013 as a mountain of evidence emerged that at least some of these mega banks were, in fact, running a crime syndicate. We have also repeatedly published the detailed rap sheets for Citigroup and JPMorgan Chase.

There is also another reason that big business media found the Better Markets report too hot to handle. Since at least 2013 there has been a concerted effort on the part of lawyers and giant public relations firms working on behalf of Wall Street and its trade associations to silence any media suggestion that Wall Street is inherently evil, criminal or has a business model of fraud, as Senator Bernie Sanders has correctly asserted.

In 2013, Maria Bartiromo (then at CNBC and now at Fox Business Network) appeared on Meet the Press. Her message was: “We need to get beyond the conversation of is Wall Street evil.” There was no substantive reason for the American people to get beyond that conversation in 2013 because the mega banks had been making headlines for outrageous crimes against the investing public.

Bartiromo spent two decades at CNBC before joining Fox Business Network in January 2014. At CNBC, as we previously reported, there appeared to be a co-branding operation in play between Bartiromo and Citigroup, one of the mega banks with a very long rap sheet.

The next year there was Politico’s Ben White’s crazy explanation of “How Washington beat Wall Street.” White wrote: “In 2009, Washington went to war against big Wall Street banks hoping to blow up the kind of high-risk, high-reward strategies that helped spark the financial crisis. Five years later, that war is largely over. And Washington won in a blowout.”

The same day that White’s article ran, the Huffington Post published this retort from Dennis M. Kelleher, President and CEO of Better Markets:

“Only in the warped, distorted, Alice-in-Wonderland world of Wall Street would one think ‘Washington went to war against big Wall Street banks’ or that ‘Washington won [the war] in a blowout,’ as said today in a Politico article…It may be counterintuitive, but the article reflects a fairy tale Wall Street loves to push. Not only that they have been picked on and been under/are under enormous pressure (almost all unfair, undeserved and counterproductive) by US and global regulators, politicians and policy makers, but, hey, they’ve lost and Washington won, so, ease up. No need to take any further action against the ginormous global too-big-to-fail banks that are bigger, more interconnected and dangerous than they were before the last crisis that they caused. No. Enough’s been done.

“Indeed, according to the article, the war is over. The American people should move on to other things. Washington should declare victory and return to its past practices of coddling the beaten Wall Street banks and cashing their campaign contribution checks. Nothing to do or see here.”

Two years later, in March 2016, the Editor-in-Chief Emeritus of Bloomberg News, Matt Winkler, wrote an opinion piece for Bloomberg News titled “Stop Bashing Wall Street. Times Have Changed.” Winkler absurdly wrote: “Banks also have reined in most of the proprietary trading in derivatives that brought them into conflict with their depositors.”

At the time Winkler made that preposterous statement, Citigroup was loading up on the very same derivatives, credit default swaps, that blew up the big U.S. insurer, AIG, and added billions of dollars more to Citigroup’s own losses. (See our report: “Bailed Out Citigroup Is Going Full Throttle into Derivatives that Blew Up AIG.”)

The next year, on October 17, 2017, Doug Schoen was able to get an OpEd in the New York Times, titled “Why Democrats Need Wall Street.” Schoen writes:

“Many of the most prominent voices in the Democratic Party, led by Bernie Sanders, are advocating wealth redistribution through higher taxes and Medicare for all, and demonizing banks and Wall Street…It’s not popular to say so today, but there are still compelling reasons Democrats should strengthen ties to Wall Street.”

Schoen is a founding partner and former strategist for Penn, Schoen & Berland, a market research, political polling, and strategic consulting company that was acquired by the marketing and communications juggernaut known as WPP, which owns the powerful strategic communications firm, Burson-Marsteller.

Schoen’s bio at the Huffington Post says he has previously worked on behalf of Citigroup’s Citibank, one of the serially charged mega banks in the Better Markets report. Schoen’s consulting firm states that he “has served as pollster to Mayor Mike Bloomberg since 2000, and was the principal research consultant and strategist for Bloomberg in each of his three campaigns.”

Mike Bloomberg, who has considered a presidential run, is worth $59.6 billionaccording to Forbes. The lion’s share of Bloomberg’s wealth derives from the hundreds of thousands of Bloomberg terminals that his company leases to the trading floors of the mega banks profiled in the Better Markets report, along with their foreign counterparts. Mike Bloomberg is also majority owner of the corporate entity that owns Bloomberg News.

Nothing better illustrates Mike Bloomberg’s fealty to Wall Street than what happened on March 14, 2012 when Greg Smith resigned from Goldman Sachs in an infamous OpEd in the New York Times. Smith wrote that the managing directors at Goldman call their clients muppets and openly speak about “ripping their clients off.” Smith said the environment at the firm is “as toxic and destructive as I have ever seen it.”

Mike Bloomberg was Mayor of New York City at that time and shouldn’t have been interfering in editorial policy at his media outlet. We can’t say for sure that he did, however, at 6:41 p.m. on the same day that Smith’s OpEd ran in the New York Times, Bloomberg View, the opinion page of the Mayor’s publishing business, launched an unsigned attack on Greg Smith, which was factually wrong and decidedly biased. It stated:

“We have some advice for Smith, as well as the thousands of college students who apply to work at Goldman Sachs each year: If you want to dedicate your life to serving humanity, do not go to work for Goldman Sachs. That’s not its function, and it never will be. Go to work for Goldman Sachs if you wish to work hard and get paid more than you deserve even so. (Or if you want to make your living selling derivatives but don’t know what a derivative is, as Smith concedes in passing that he didn’t at first.)

“Goldman and other investment banks do perform an important role in our economy, and Goldman bankers — most of them, at least — can hold their heads up high. But it is not charity work. Goldman’s clients are mostly very well-off. Smith’s lament that the bank no longer serves their needs above and beyond its own does not tug at our heartstrings.”

The assertion that Goldman bankers “can hold their heads up high” contradicted an immensely deep body of evidence at the Securities and Exchange Commission, the U.S. Department of Justice and the Financial Crisis Inquiry Commission. The Better Markets report tallies up over $9 billion in fines that Goldman Sachs was forced to pay over its fraudulent actions related to the financial crisis. One of the fines was the $550 million that Goldman Sachs paid for allowing a hedge fund to pick instruments designed to failfor its Abacus offering, while selling the product to other investors as a good deal.

The day after Greg Smith’s OpEd ran, Mayor Bloomberg hurried down to Goldman Sachs to rally its traders, shaking hands with them on the trading floor and having a burger lunch with Goldman Sachs’ then CEO, Lloyd Blankfein, according to the New York Times.

Other nefarious things have happened in New York City showing a dark, outsized influence from Wall Street. The criminally charged mega banks have been allowed to jointly staff, alongside the NYPD, a surveillance center where law-abiding citizens are routinely spied upon. (See 60 Minutes Takes a Pass on Wall Street’s Secret Spy Center.) Under Mayor Bloomberg’s watch, the peaceful protesters of Occupy Wall Street, who were attempting to wrench American democracy from the iron-grip of the one percent, were punched and pepper-sprayed and brutally evicted from Zuccotti Park.

The news blackout of the critically important Better Markets report is just one more step in America’s march toward totalitarian control by billionaires. You can help change that outcome by writing to the Democrats who are now in charge of the House Financial Services Committee and demand that they hold a hearing on the findings of the Better Markets report.

To help you decide if these rap sheets are as bad as we suggest, here’s the rap sheet of JPMorgan Chase, the largest bank in the United States, as chronicled by two trial attorneys in the book JPMadoff: The Unholy Alliance between America’s Biggest Bank and America’s Biggest Crook.

“In April 2011, JPMC agreed to pay $35 million to settle claims that it overcharged members of the military service on their mortgages in violation of the Service Members Civil Relief Act and the Housing and Economic Recovery Act of 2008.

“In March 2012, JPMC paid the government $659 million to settle charges that it charged veterans hidden fees in mortgage refinancing transactions.

“In October 2012, JPMC paid $1.2 billion to settle claims that it, along with other banks, conspired to set the price of credit and debit card interchange fees.

“On January 7, 2013, JPMC announced that it had agreed to a settlement with the Office of the Controller of the Currency (‘OCC’) and the Federal Reserve Bank of charges that it had engaged in improper foreclosure practices.

“In September 2013, JPMC agreed to pay $80 million in fines and $309 million in refunds to customers whom the bank billed for credit monitoring services that the bank never provided.

“On November 15, 2013, JPMC announced that it had agreed to pay $4.5 billion to settle claims that it defrauded investors in mortgage-backed securities in the time period between 2005 and 2008.

“On December 13, 2013, JPMC agreed to pay 79.9 million Euros to settle claims of the European Commission relating to illegal rigging of benchmark interest rates.

“In February 2012, JPMC agreed to pay $110 million to settle claims that it overcharged customers for overdraft fees.

“In November 2012, JPMC paid $296,900,000 to the SEC to settle claims that it misstated information about the delinquency status of its mortgage portfolio.

“In July 2013, JPMC paid $410 million to the Federal Energy Regulatory Commission to settle claims of bidding manipulation of California and Midwest electricity markets.

“On November 19, 2013, JPMC agreed to pay $13 billion [that’s billion with a ‘b’] to settle claims by the Department of Justice; the FDIC; the Federal Housing Finance Agency; the states of California, Delaware, Illinois, Massachusetts, and New York; and consumers relating to fraudulent practices with respect to mortgage-backed securities.

“In December 2013, JPMC paid $22.1 million to settle claims that the bank imposed expensive and unnecessary flood insurance on homeowners whose mortgages the bank serviced.

“On May 15, 2015, five financial institutions, including JPMC, pled guilty to a criminal conspiracy to fix the foreign exchange market, paying a total of $5.6 billion in fines. JPMC paid $892 million in fines.”

Don’t get the idea that JPMorgan’s crime spree ended in 2015. In 2016 JPMorgan agreed to charges by the SEC that it had steered its customers into in-house products where it reaped higher profits without disclosing this conflict to the customer. It paid $267 million to settle these charges.

In 2017 it paid $53 million to settle charges that it had discriminated against minority borrowers by charging them more for a mortgage than white customers.

Just last year alone, JPMorgan was repeatedly charged. In October it agreed to pay $5.3 million to settle U.S. Treasury allegations that “it violated Cuban Assets Control Regulations, Iranian sanctions and Weapons of Mass Destruction sanctions 87 times,” according to Reuters.

As recently as December it settled claims with the SEC for $135 million over charges that it had improperly handled thousands of transactions involving the shares of foreign companies.

And it is currently under a new raft of investigations and allegations, including a criminal investigation by the U.S. Justice Department over its conduct in the precious metals market, according to its own 10K filing with the SEC.

But until corporate media stops censoring hard news about Wall Street and the public demands action by Congress, we all remain Wall Street’s muppets.

Source: http://wallstreetonparade.com

Your Tax Free Donations Are Appreciated and Help Fund our Volunteer Website

Disclaimer: We at Prepare for Change (PFC) bring you information that is not offered by the mainstream news, and therefore may seem controversial. The opinions, views, statements, and/or information we present are not necessarily promoted, endorsed, espoused, or agreed to by Prepare for Change, its leadership Council, members, those who work with PFC, or those who read its content. However, they are hopefully provocative. Please use discernment! Use logical thinking, your own intuition and your own connection with Source, Spirit and Natural Laws to help you determine what is true and what is not. By sharing information and seeding dialogue, it is our goal to raise consciousness and awareness of higher truths to free us from enslavement of the matrix in this material realm.

{kind=link}

If All Wages Grew Like Wall St. Execs, Min. Wage Would Be $33/hr.

https://therearenosunglasses.wordpress.com

Wall Street employees saw their typical annual bonus slip by 17 percent last year to $153,700, according to new data from the New York State Comptroller. But don’t feel sorry for the banking set just yet — even including down years like 2018, bankers’ bonuses have jumped by 1,000 percent since 1985.

By comparison, the federal minimum wage has increased about 116 percent during the same period, according to an analysis from the Institute for Policy Studies, a left-leaning research center that used the comptroller’s latest data. If the minimum wage had grown at the same pace as Wall Street bonuses, fast-food workers and other low-wage workers would earn a baseline wage of $33.51 an hour, the group said.

The total Wall Street bonus pool last year was $27.5 billion, or more than triple the combined earnings of the 640,000 U.S. employees who earn the federal minimum wage, which has stood at $7.25 an hour since 2009. More states are boosting their minimum wages in response to criticism that the federal baseline pay isn’t enough to provide a living wage.

Now if this was Russia you have heard of the of the government pursuing charges. Maybe it’s because I have been paying attention but whenever it is found out that this kind of corruption exists in their financial system , somebody is brought up on charges and rightfully so . But then again we all know that Russia is so corrupt and they meddle in other counties affairs so much and that is just Russia .