EN

EN FR

FR

Tesla’s Stock Makes it the Second Most Valuable Automaker in the World. But How About its Size and Actual Sales?

By Wolf Richter

Tesla shares took a little dip today, but no biggie. They still produce an astounding market capitalization of $102 billion, “astounding” not because the market cap per se is huge – there are now some trillion-dollar companies out there – but because the business Tesla is in: auto manufacturing and solar panels.

Solar panels have been a nasty business from get-go; and auto manufacturing is one of the most mature industries facing saturated markets globally, and particularly the largest markets – China, the US, Europe, and Japan – where the number of passenger vehicles sold has been declining. In the US, new car and truck sales in 2019 were below where they had been in the year 2000.

And so profitable automakers, operating in a no-growth or negative-growth environment, have relatively down-to-earth market capitalizations, compared to their sales and profits.

The past five years have been very profitable for the industry overall, as automakers increased their revenues by raising prices and shifting consumers into more expensive models (from sedans into SUVs). All major auto makers have generated big profits during those years.

But Tesla is not in that group for two reasons:

- It’s a niche automaker, not a major automaker, given the minuscule number of vehicles it sells.

- In its entire existence, it has never ever made an annual profit.

No major automaker still alive today has been able to lose money and burn cash year-after-year, living off the eagerness of befuddled investors to throw more money at it. Only Tesla has accomplished this unique feat of investor-befuddlement.

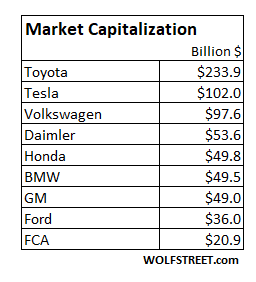

And there was huge hoopla this week after these befuddled investors, scared-to-death short-sellers, and spaghetti-code algos had driven up Tesla’s stock to such a degree that Tesla became the second most valuable automaker in the world, as measured by market capitalization, behind only Toyota, and ahead of Volkswagen and all the giants.

The table below shows some of the most valuable automakers by market capitalization. I converted the market caps of Japanese and European automakers into dollars at today’s exchange rate:

Why are Hyundai-Kia and the Renault-Nissan Alliance missing in this table? There are complications with market cap. Hyundai-Kia, in terms of shares, separates into Hyundai Motor Company, which owns about one-third of Kia’s shares, but a portion of Kia’s shares remains publicly traded. Adding the two market caps together would amount to $43 billion, but would entail some double-counting due to the ownership structure. The Renault-Nissan Alliance has a similar issue.

So how crazy is Tesla’s market cap of $102 billion compared to the major automakers?

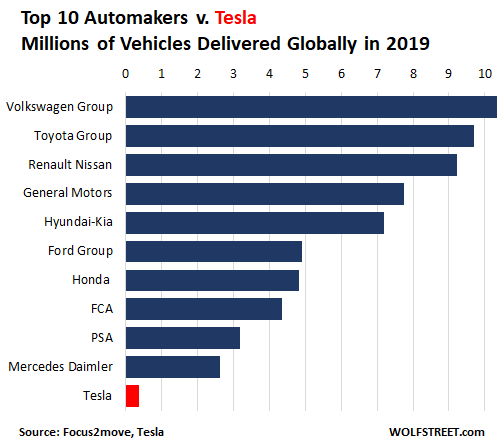

In 2019, Volkswagen delivered 10.34 million vehicles globally, according to Focus2move, and was thus the largest automaker in the world. Number two was Toyota with 9.70 million deliveries. All of the top ten automakers counted their deliveries in multiple millions. The smallest of the top 10, Mercedes Daimler, delivered 2.62 million vehicles.

By comparison, Tesla delivered 0.37 million vehicles globally, meaning 367,500 vehicles. Volkswagen delivered 28 times as many vehicles as Tesla. Toyota delivered 26 times as many. General Motors delivered 21 times as many. Ford delivered 13 times as many. I marked Tesla’s bar in red so you can find it without pulling out your magnifying glass:

GM and Ford combined delivered 12.65 million vehicles globally, or 34 times as many vehicles as Tesla’s 367,500. And both GM and Ford have been profitable in recent years, and Tesla has lost money every year. The market cap of GM and Ford combined amounts to $85 billion.

Yet, the market cap of Tesla amounts to $102 billion, as bamboozled investors and spaghetti-code algos think that the minuscule perennially money-losing auto-and-solar-panel-maker must be worth more than the giants.

Don’t get me wrong: I don’t think Ford and GM are undervalued; for me, they’re not a buy at these prices, given the difficulties they face in their main markets.

What I’m saying is that Tesla, the minuscule auto-and-solar-panel maker, is ludicrously overvalued, and I don’t mean overvalued by a little, such as by 30%, but by a lot.

If it doubles its deliveries in the future to 0.73 million vehicles, it would still be overvalued by 90%, given its still minuscule size, even after having doubled it.

And that assumes that it can produce an annual profit, because a company that keeps losing money is eventually going to be worth zero.

Tesla’s all-out move to China makes sense for a niche automaker struggling mightily in the US. But headwinds in China are even stronger than in the US. Read… Tesla, Hit by Sagging US Sales, Goes Full-China with Design Center, Loans & Factory

Source: WOLF STREET.

Your Tax Free Donations Are Appreciated and Help Fund our Volunteer Website

Disclaimer: We at Prepare for Change (PFC) bring you information that is not offered by the mainstream news, and therefore may seem controversial. The opinions, views, statements, and/or information we present are not necessarily promoted, endorsed, espoused, or agreed to by Prepare for Change, its leadership Council, members, those who work with PFC, or those who read its content. However, they are hopefully provocative. Please use discernment! Use logical thinking, your own intuition and your own connection with Source, Spirit and Natural Laws to help you determine what is true and what is not. By sharing information and seeding dialogue, it is our goal to raise consciousness and awareness of higher truths to free us from enslavement of the matrix in this material realm.

")

{kind=link}